Only 6% of all South Africans can retire comfortably while 17% rely on the government pension of only R1 900 per month. Which one do you want to be?

Planning for your retirement and starting to save towards it should happen as soon as you start working. Your working life can be anywhere between 40-45 years and that equates to between 480 and 540 pay cheques.

Now, if you retire at age 65 and live until 80 you would have to make provision for 15 yearly pay cheques. You should aim to save towards a retirement income of at least 75% of your final salary to live comfortably in your golden years.

Saving towards your retirement will mean less disposable monthly income but before you know it, you will be used to a little less money per month. Your retirement savings will be your lifeline when in retirement and the fact that you can lower your taxable income while working, by saving for your retirement is a no brainer. And who does not want to save on their tax bill?

Let’s look at what the tax benefits are when contributing towards YOUR retirement.

Contributions to retirement funds are tax deductible, within the following limits. The maximum tax deduction per year is limited to 27.5% of your taxable income, subject to an annual maximum of R350 000. From 1 March 2016, tax deductions for retirement savings increased from 15% to 27.5%, which means you can now save more towards YOUR retirement and get more back from SARS.

If you are a member of a company pension or provident fund, you can still set up an individual retirement annuity to supplement your existing contributions and maximise your tax savings. It is never too late to start saving for YOUR retirement.

Let’s look at the following scenario of how Joe can reduce his tax impact (Tax rebate calculations are pulled from the SARS 2021/2022 tax tables, find it here):

Joe Soap who is 35 years’ old, earns a salary of R480 000 per annum and is contributing 15% of his income towards his retirement. In the process of increasing to the maximum of 27.5%.

Example 1: Joe Soap’s retirement savings contributions and payable tax from 1 March 2021 to 28 February 2022 saving at 15%

Annual Salary: R480 000

Retirement contribution: R480 000 x 15% = R72 000 P/A

Taxable Income: R480 000 – R72 000 = R408 000

Annual tax paid: R70 532 + [31% x (R408 000 – R337 800)] = R92 294 – R15 714 (primary rebate) = R76 580

Example 2: Let’s assume Joe Soap is contributing R0 towards his retirement fund.

Retirement contribution: R0

Taxable income: R480 000 – R0 = R480 000

Annual tax paid: R110 739 + [36% x (480 000 – 467 500)] = R115 239 – R15 714 (primary rebate) = R99 525

Example 3: Lastly, Joe Soap’s retirement savings contributions and tax from 1 March 2021 to 28 February 2022 should he increases his contributions to 27.5%

Annual Salary: R480 000

Retirement contribution: R480 000 x 27.5% = R132 000 P/A

Taxable income: R480 000 – R132 000 = R348 000

Annual tax paid: R70 532+ [31% x (R348 000 – R337 800)] = R73 694 – R15 714 (primary rebate) = R57 980

By taking advantage of the tax deduction limits, Mr. Joe Soap can save an additional R18 600 on his annual tax return by increasing his contributions from 15% to 27,5% from example 1 to Example 3. This amount will be going towards your retirement savings per year rather than losing it to government tax.

From not contributing at all towards his retirement to contributing 27,5% Joe Soap’s tax saving is R41 545, from example 2 to example 3. SARS is funding almost 42% of his retirement contributions for the year. You too could benefit from this by starting to save today. Also, any future growth on your retirement funds is also tax free.

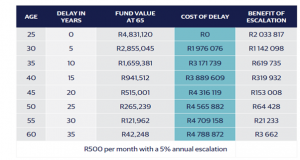

So don’t delay it might just cost you to cut down on your retirement plans. The following table demonstrates the cost of delay and how 5 years can have significant impacts on the funds you have available at retirement.

Author:

Rene Zietsman: Financial Advisor and Unit Leader of IWCP Cedarwood.